|

amortization.com Ltd. 905-639-0374

|

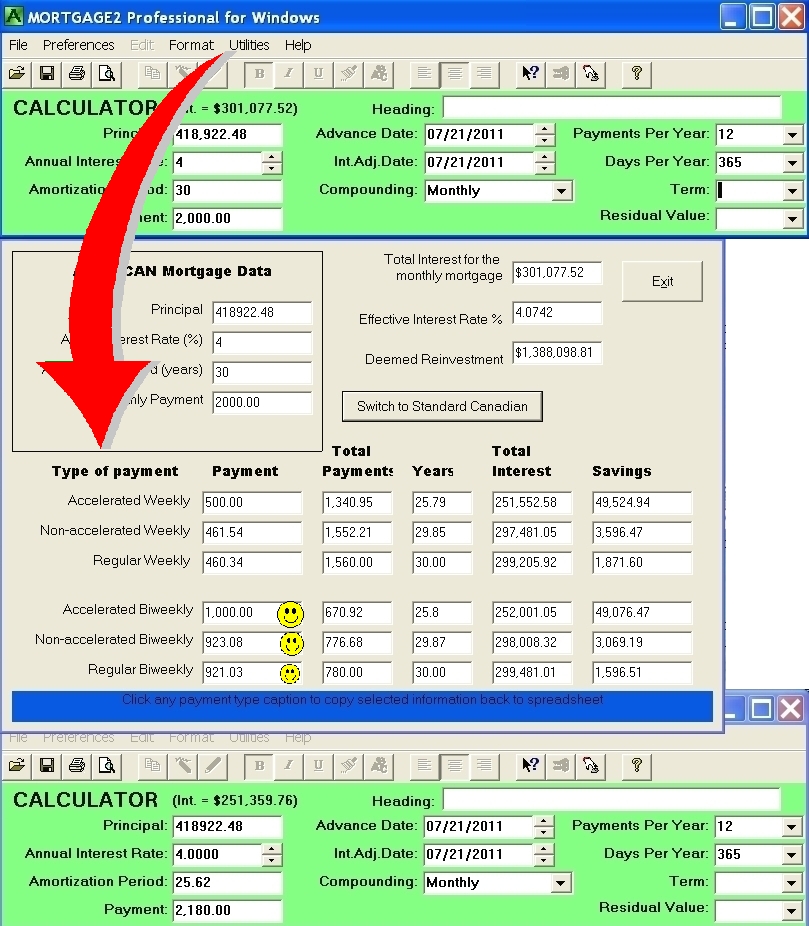

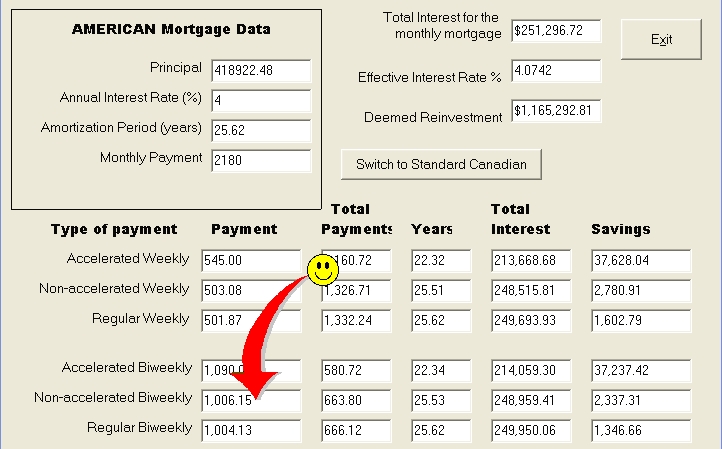

Caveat Emptor, "Let the buyer beware". If you are an American and have a mortgage its unfortunate that you cannot get a Canadian biweekly payment mortgage. Canadian Banks and the Canadian borrowers went through the biweekly (and weekly) mortgage debate in 1984 and the issue was settled long ago. Fact, the best way to minimize interest costs on a mortgage is to pay back the loan ASAP. This simply means the weekly is the best and is better than the biweekly which in turn is better than the monthly payment mortgage! Canadian Banks offer a true biweekly payment mortgage. Americans should be aware of smoke and mirror tactics that some US Banks utilize to fool you into thinking you are getting a deal with their particular biweekly payment mortgage. Canadian biweekly payment mortgages are calculated and amortized exactly the same way as regular monthly payment mortgages. There is nothing new, under the sun, concerning a biweekly payment mortgage. The MIGHTY BARGAIN HUNTER web site was brought to my attention by an astute American reader. Two items bothered me. The first was the web site’s statement about biweekly payment mortgages. The statement was confusing and riddled with faulty “logic”. For example, it stated that increasing your monthly payment by 9% is “almost exactly the same thing” as the accelerated biweekly payment mortgage. This is not true! The author of those words is not comparing the same cash flows. The writer is comparing apples with oranges. When performing any mathematical analysis of two mortgages one must always compare the same cash flow. The writer obviously does not understand the time value of money or the present value future value concept. I use an example mortgage of $418,922.48 amortized for 30 years using a 4% annual interest rate. I purposely chose these numbers so the monthly payment would be exactly $2000 and thus the accelerated biweekly would be $1000. Increasing the monthly payment by 9% to $2180 instead of paying $2000 per month saves $49,717.76 in interest (301,077.52 – 251,359.76). ACCELERATED BIWEEKLY NON ACCELERATED BIWEEKLY REGULAR BIWEEKLY If your still not convinced a biweekly payment mortgage is the way to go then consider the non accelerated biweekly payment of $1,006.15 every two weeks instead of the $2,180 per month. That’s the same yearly cash flow of $26,160 but it is taken out of your account biweekly instead of monthly and again you save free money of $2,337.31 over the 25.53 years for doing absolutely nothing. A new fridge or stove perhaps? The second thing that bothered me and it should especially upset Americans, is the unethical and confusing practices of some US lenders concerning how “additional principal” payments are handled. In Canada, any amount of money paid in excess of interest due at the end of a period of time is immediately applied towards reducing the principal (obviously the mortgage must be open with no penalties). In fact some Canadian lenders take your taxes each month or every 14 days and apply it towards paying down the principal and then add the paid taxes on to the balance at the end of the appropriate time. This lets you use your tax payments to help lower your interest costs. These are some of the fair, ethical and common sense perks that some Canadian banks follow. Perhaps that is one of the many reasons why Canadian Banks did not get sucked into the financial black hole during the 2008 US banking collapse. Canadian Banks still have pimples and worts buts that is a topic for another day. Last Caveat, a biweekly amortization schedule is essential because the interest portion of the very first biweekly payment divided by the initial Principal (amount borrowed) gives you the biweekly interest factor, The biweekly interest factor determines how the interest is calculated at the end of each 14 day period. Lenders do not always disclose their biweekly factor. The larger the biweekly interest factor the more interest you pay! Knowing the APR number as a percentage or a modified APR is not enough. The cost of borrowing number WILL NOT DIVULGE the potential variation in total interest costs. The cost of borrowing that’s reported influences the stated APR but does not indicate the numerical value of the informative interest factor, that determines the total interest costs.

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}

{kind=link}

{kind=link}